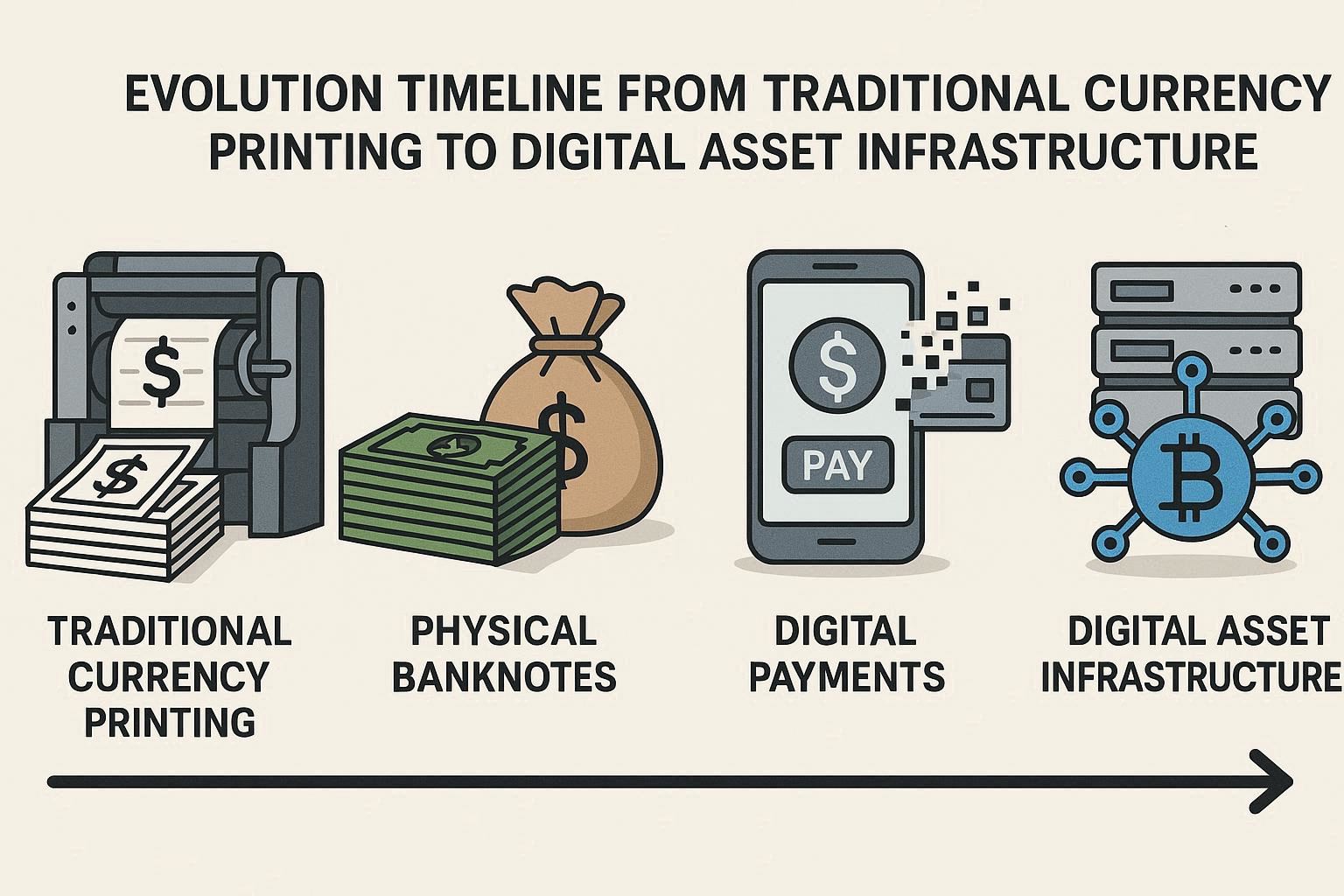

Introduction: The Transformation of Monetary Sovereignty

For centuries, the power to issue currency has been the cornerstone of state sovereignty. The exclusive right to create money, control its supply, and regulate its circulation represented one of the most fundamental expressions of governmental authority. This monopoly over monetary issuance enabled nations to finance wars, stimulate economies, and exercise control over their citizens’ economic lives. Yet we are now witnessing a profound transformation in the nature of sovereign financial power—a shift from the traditional prerogative of printing money to the emerging imperative of controlling digital asset custody.

This evolution is not merely a technological upgrade of existing systems. It represents a fundamental reconceptualization of what monetary sovereignty means in an increasingly digitalized and decentralized world. As cryptocurrencies, stablecoins, tokenized assets, and central bank digital currencies (CBDCs) proliferate, the question of who holds, controls, and validates digital assets becomes as critical as who issues currency. The battleground of financial sovereignty has expanded from the printing press and central bank reserves to encompass blockchain networks, cryptographic keys, and digital custody infrastructure.

Understanding this transition is essential for policymakers, financial institutions, and citizens alike. The frameworks established today will determine the balance of power between states, corporations, and individuals for decades to come. Will nations successfully reassert their financial sovereignty in the digital age, or will they find themselves competing with private entities that control the infrastructure of the new financial system?

The Historical Foundation: Monetary Issuance as Sovereign Power

To appreciate the magnitude of the current transformation, we must first understand the historical significance of monetary issuance. The exclusive right to create money emerged as a defining characteristic of the modern nation-state during the Renaissance and crystallized with the establishment of central banking in the 17th and 18th centuries. This monopoly served multiple purposes: it provided governments with seigniorage revenue, enabled macroeconomic management, and created a unified medium of exchange that facilitated commerce and taxation.

The twentieth century saw the apotheosis of state monetary power. The abandonment of the gold standard, the rise of fiat currency, and the development of sophisticated central banking tools gave governments unprecedented control over their monetary systems. Central banks could expand or contract money supply, influence interest rates, and intervene in financial markets to achieve policy objectives. This power became so fundamental to state authority that “monetary sovereignty” became synonymous with national independence.

However, this system always depended on certain structural conditions: closed capital accounts, limited cross-border flows, and the absence of viable alternatives to state-issued currency. As globalization accelerated and technology advanced, these conditions began to erode. International financial integration meant that capital could flee at the first sign of monetary instability. The rise of foreign exchange markets enabled citizens to dollarize their savings even in countries with strict capital controls. The state’s monetary monopoly, while still powerful, was no longer absolute.

The 2008 financial crisis exposed another vulnerability: the interdependence of monetary systems meant that even the most powerful central banks needed international coordination to prevent systemic collapse. The Federal Reserve’s dollar swap lines to foreign central banks demonstrated that monetary sovereignty was increasingly relative rather than absolute. This context set the stage for the disruption that would follow.

The Cryptocurrency Challenge: Decentralization Meets Sovereignty

The emergence of Bitcoin in 2009 represented an unprecedented challenge to state monetary sovereignty. For the first time, a functional monetary system operated entirely outside governmental control, with issuance governed by algorithmic rules rather than policy decisions. While early skeptics dismissed Bitcoin as a curiosity for libertarians and criminals, its persistence and growth forced serious engagement with its implications.

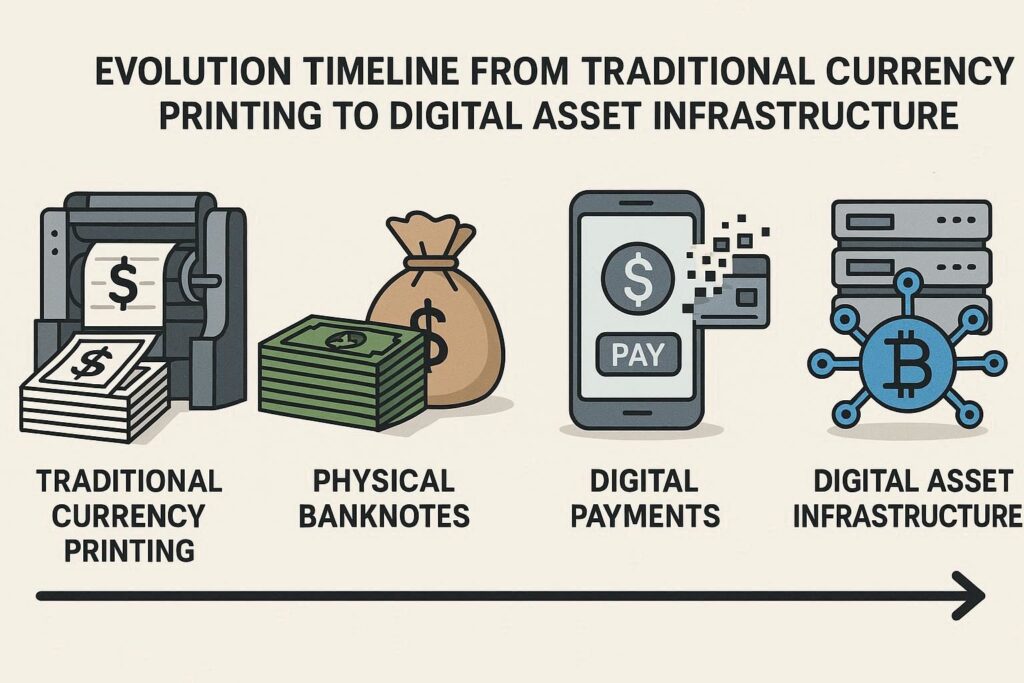

Cryptocurrencies fundamentally challenge the state monopoly on money by offering alternative stores of value and mediums of exchange that function independently of governmental approval. More significantly, they introduced concepts of custody and control that diverge radically from traditional finance. In the cryptocurrency paradigm, possession of private keys constitutes ownership—a principle captured in the saying “not your keys, not your coins.” This cryptographic approach to asset control operates outside the legal and institutional frameworks through which states traditionally assert financial sovereignty.

The proliferation of thousands of cryptocurrencies and the emergence of decentralized finance (DeFi) platforms have created parallel financial ecosystems that process hundreds of billions of dollars in transactions outside traditional banking channels. These systems don’t merely compete with state currencies; they offer entirely different models of monetary organization based on code rather than law, cryptographic proof rather than institutional trust, and decentralized networks rather than centralized authorities.

Nations have responded to this challenge with varying strategies. China banned cryptocurrency trading and mining while accelerating development of its digital yuan. The United States has pursued a regulatory approach, treating cryptocurrencies as securities or commodities subject to existing financial rules while debating comprehensive crypto-specific legislation. The European Union’s Markets in Crypto-Assets (MiCA) regulation represents an attempt to create a coherent framework that protects consumers while permitting innovation. Meanwhile, smaller nations like El Salvador have embraced Bitcoin as legal tender, attempting to leverage crypto adoption for economic development and financial inclusion.

The Custody Revolution: Where Value Resides in Digital Systems

The shift from physical to digital assets has fundamentally altered the question of custody. In traditional finance, custody is a service provided by banks and specialized institutions that hold assets on behalf of clients. The custody relationship is governed by contracts, regulated by law, and ultimately enforceable through state power. A bank holding your money doesn’t physically possess it in a vault labeled with your name; rather, it maintains database entries reflecting your claim on the institution’s assets.

Digital assets, particularly cryptocurrencies, introduce a new custody paradigm. Value doesn’t reside in accounts maintained by institutions but in addresses on distributed ledgers, accessible only through private cryptographic keys. The entity possessing these keys has effective control over the assets, regardless of legal claims or institutional relationships. This technical reality creates profound challenges for traditional concepts of ownership, inheritance, bankruptcy, and law enforcement.

The custody question becomes even more complex with tokenized real-world assets—securities, real estate, commodities, and other valuable items represented as digital tokens on blockchains. Who actually controls these assets? The holder of the private keys? The legal owner according to traditional property records? The institution that issued the tokens? The smart contract that governs their transfer? These questions don’t have clear answers, and different jurisdictions are developing divergent approaches.

States are recognizing that controlling digital asset custody infrastructure may be more important than traditional monetary issuance in determining their future financial sovereignty. If citizens increasingly hold wealth in digital assets, and if foreign entities control the custody infrastructure for those assets, then a nation’s effective sovereignty over its economy diminishes regardless of its control over currency issuance. This realization is driving dramatic changes in regulatory priorities and strategic investments.

Central Bank Digital Currencies: Reasserting Sovereign Control

Central bank digital currencies represent the state’s most direct response to the challenges posed by cryptocurrencies and private digital assets. CBDCs are digital forms of sovereign currency issued and controlled by central banks, combining the technological advantages of digital assets with the authority and stability of state money. More than 130 countries, representing 98% of global GDP, are now exploring CBDCs, with several already in advanced pilot or implementation stages.

The motivations for CBDC development vary across nations but generally include maintaining monetary sovereignty in a digitizing world, improving payment system efficiency, promoting financial inclusion, and countering the threat of private cryptocurrencies or foreign digital currencies dominating domestic markets. China’s digital yuan development, for instance, is explicitly linked to concerns about maintaining monetary sovereignty and reducing dependence on dollar-denominated international payment systems.

However, CBDCs represent more than simply digitizing existing currencies. Their design choices carry profound implications for privacy, state surveillance, financial inclusion, and the balance of power between governments, banks, and citizens. A retail CBDC that allows direct central bank accounts for all citizens could disintermediate commercial banks, fundamentally restructuring the financial system. Alternatively, a wholesale CBDC used only for interbank settlements might enhance efficiency without disrupting existing structures.

The custody question for CBDCs is particularly significant. Will citizens hold their digital currency in wallets they control, similar to cash or cryptocurrencies? Or will CBDCs function more like traditional bank accounts, with institutions mediating access? Will transactions be private like cash or traceable like credit cards? These design decisions determine whether CBDCs reinforce or undermine individual financial autonomy, and whether they enhance or threaten civil liberties.

China’s digital yuan pilots demonstrate one model: a centralized system where the central bank maintains ultimate control while using commercial banks and payment platforms for distribution. The European Central Bank’s digital euro project envisions a different balance, with stronger privacy protections and limits on central bank access to transaction data. These varying approaches reflect different political systems, cultural values, and strategic priorities—but all represent attempts to reassert sovereign monetary control in the digital age.

The Custody Infrastructure Battle: Private vs. Public Control

As digital assets proliferate, the infrastructure for securing and managing them has become a critical strategic resource. Cryptocurrency exchanges, custodial wallets, institutional custody services, and decentralized protocols all compete to control this infrastructure. The entities that dominate digital asset custody wield enormous power—they can freeze accounts, monitor transactions, enforce sanctions, and ultimately determine who can participate in the digital economy.

Major technology companies and financial institutions are aggressively entering the custody space, recognizing its strategic importance. PayPal, Square, and traditional banks now offer cryptocurrency custody services. Specialized crypto custodians like Coinbase Custody and BitGo manage billions in digital assets for institutional clients. Technology giants like Facebook (now Meta) have attempted to launch their own digital currency initiatives, though regulatory pushback forced significant modifications to these plans.

This concentration of custody power in private hands concerns many governments. When a private company controls the wallet infrastructure through which millions access digital assets, it effectively becomes a financial gatekeeper with power that rivals or exceeds traditional banks. Yet these private custodians often operate across borders, making them difficult to regulate and creating opportunities for regulatory arbitrage.

States are responding by asserting jurisdiction over custody infrastructure. Regulations increasingly require digital asset custodians to obtain licenses, implement know-your-customer procedures, report suspicious transactions, and comply with sanctions. The EU’s MiCA regulation includes specific provisions for crypto-asset service providers, including custodians. The United States requires money transmitter licenses at both federal and state levels, creating a complex compliance landscape.

Some nations go further, requiring that custody of digital assets belonging to their citizens occur within their jurisdiction, under supervision of domestic regulators. This “custody sovereignty” approach mirrors data localization requirements in the technology sector. It aims to ensure that states can enforce their laws over digital assets and prevent foreign governments or companies from exercising undue influence over their citizens’ financial lives.

However, the decentralized nature of cryptocurrency custody complicates these efforts. Self-custody—where individuals hold their own private keys—operates entirely outside institutional frameworks. While this empowers individuals and protects privacy, it also limits state ability to enforce laws, collect taxes, or prevent illicit activity. The tension between enabling self-custody (which enhances financial freedom) and requiring institutional custody (which enables regulation) represents one of the central policy dilemmas in digital asset governance.

Stablecoins: Private Money and Public Authority

Stablecoins—cryptocurrencies designed to maintain stable value by pegging to fiat currencies or other assets—represent a particularly interesting challenge to monetary sovereignty. They combine the technological advantages of cryptocurrencies with the stability of traditional currencies, making them potentially more viable for everyday transactions than volatile assets like Bitcoin. Stablecoin transaction volumes now exceed trillions of dollars annually, with Tether (USDT) and USD Coin (USDC) dominating the market.

The rapid growth of dollar-denominated stablecoins creates a paradox for U.S. monetary sovereignty. On one hand, these instruments extend dollar hegemony into the digital realm, potentially strengthening American financial power. On the other hand, they represent private entities issuing dollar-equivalent instruments outside traditional banking regulation, creating systemic risks and reducing policy control.

The custody of assets backing stablecoins raises critical sovereignty questions. Where are the reserves held? In what instruments? Under whose jurisdiction? When Circle, the issuer of USDC, holds billions in treasury securities backing its stablecoin, those assets must be custodied somewhere—typically with U.S.-based institutions subject to U.S. law. This creates dependencies and vulnerabilities that affect the stablecoin’s reliability and the sovereignty of nations whose citizens use it.

Different countries are adopting divergent regulatory approaches to stablecoins. The United States debates whether to regulate them as securities, bank deposits, or an entirely new category. The European Union’s MiCA framework creates specific rules for “asset-referenced tokens” and “e-money tokens,” requiring issuers to obtain authorization and maintain adequate reserves. Some countries, concerned about the sovereignty implications, are moving to ban or strictly limit stablecoins while accelerating their own CBDC development.

The emergence of algorithmic stablecoins—which attempt to maintain price stability through mechanisms other than asset backing—adds further complexity. While the spectacular collapse of TerraUSD in 2022 demonstrated the risks of these instruments, the concept of decentralized stable value remains appealing to those seeking alternatives to both volatile cryptocurrencies and state-controlled currencies. The regulatory treatment of such instruments will significantly impact innovation in this space and determine whether decentralized alternatives to sovereign money can viably exist.

Cross-Border Implications: Sovereignty in an Interconnected System

The digital asset revolution has profound implications for cross-border payments and international financial architecture. Traditional international money transfers involve multiple intermediaries, take days to settle, and incur significant fees. Digital assets promise near-instant transfers at minimal cost, regardless of borders. This efficiency comes, however, with challenges to the control mechanisms through which states regulate capital flows and enforce sanctions.

Many developing nations face a particular dilemma. Their citizens increasingly use cryptocurrencies to circumvent capital controls, preserve wealth against inflation, and facilitate remittances. While this provides individual benefits, it undermines the state’s ability to manage its economy and protect its currency. Lebanon, Argentina, Nigeria, and other nations with monetary instability have seen dramatic cryptocurrency adoption as citizens seek stores of value beyond unreliable national currencies.

The sovereignty implications become even more significant when considering international settlements. Currently, the SWIFT system and correspondent banking networks give certain nations—particularly the United States—extraordinary power to enforce sanctions and monitor global financial flows. A world where significant value transfers occur through cryptocurrency networks or CBDC corridors could fundamentally alter these power dynamics.

China’s Cross-Border Interbank Payment System (CIPS) and digital yuan pilots with other nations represent attempts to create alternative international settlement infrastructure, reducing dependence on dollar-denominated systems. The Bank for International Settlements’ Project mBridge, testing multi-CBDC platforms for cross-border payments, explores how nations might cooperate on digital currency infrastructure while maintaining individual sovereignty.

These developments suggest a future international financial system far more fragmented than today’s dollar-dominated order. Rather than a single global reserve currency and settlement network, we may see multiple regional or bloc-based systems, with varying degrees of interoperability. Digital assets and CBDCs could enable this fragmentation by reducing the technical barriers to alternative payment systems, while geopolitical tensions provide the motivation.

Regulatory Frameworks: Balancing Innovation and Control

The regulatory approach to digital assets directly impacts how sovereignty manifests in the custody domain. Overly restrictive regulations may drive innovation and economic activity to more permissive jurisdictions, undermining the very sovereignty regulators seek to protect. Insufficient regulation creates systemic risks, enables illicit activity, and leaves consumers vulnerable to fraud and loss.

Different jurisdictions are experimenting with various regulatory models. Switzerland has created a comprehensive “crypto valley” framework that provides legal clarity while enabling innovation. Singapore has implemented a licensing regime for digital payment token services while promoting responsible innovation. The Bahamas, seeking to position itself as a digital finance hub, offers streamlined regulatory approval for digital asset businesses.

More significant players face greater challenges in balancing competing priorities. The United States’ fragmented regulatory structure—with different agencies claiming jurisdiction over various aspects of digital assets—creates uncertainty and compliance burdens. The SEC treats many tokens as securities, the CFTC regulates cryptocurrency derivatives as commodities, FinCEN applies anti-money laundering rules as if custodians were money transmitters, and the IRS treats crypto as property for tax purposes. This complexity favors large, well-resourced firms while hindering smaller innovators.

The European Union’s MiCA regulation attempts to create harmonized rules across member states while preserving national discretion in certain areas. This approach seeks to eliminate regulatory arbitrage within Europe while maintaining competitiveness globally. The framework includes provisions for asset custody, requiring custodians to separate client assets from their own holdings, maintain adequate capital, and implement robust security measures.

Regulatory treatment of decentralized finance platforms poses particular challenges. When custody and financial services are provided through smart contracts and decentralized protocols rather than identifiable institutions, traditional regulatory approaches struggle. Who is responsible for compliance when there’s no central entity to hold accountable? How can states enforce their laws on protocols that exist as code distributed across global networks? These questions push regulators toward innovative approaches like focusing on points of interface between decentralized protocols and traditional finance, or holding protocol developers accountable for design choices.

The Future of Financial Sovereignty: Emerging Paradigms

As we look toward the future, several competing visions of financial sovereignty are emerging. The first envisions enhanced state control through CBDCs and comprehensive regulation of digital asset infrastructure. In this scenario, governments successfully adapt their monetary sovereignty to the digital age, maintaining control over custody infrastructure and using technology to strengthen rather than weaken their authority.

A second vision sees a more decentralized future where individuals have greater financial autonomy through self-custody of digital assets, with states playing a reduced but still significant role in providing stable currencies and regulatory frameworks that protect consumers without constraining innovation. This model would redefine sovereignty as enabling rather than controlling, with states earning their monetary privilege through providing stable value rather than asserting legal monopoly.

A third possibility involves corporate dominance, where major technology and financial companies control digital asset custody infrastructure, with states becoming increasingly dependent on these platforms to exercise financial sovereignty. This scenario, while concerning from a democratic accountability perspective, might emerge if private entities prove more capable than governments of building the infrastructure users actually want to use.

The most likely outcome involves elements of all three visions, varying across different nations and regions based on their particular circumstances, values, and capabilities. What’s certain is that the locus of sovereign financial power is shifting from the exclusive capacity to issue currency toward the ability to control, regulate, and secure digital asset custody infrastructure.

This shift requires nations to develop new capabilities. They must build or oversee reliable digital custody infrastructure. They must craft regulations sophisticated enough to address digital assets’ unique characteristics while avoiding stifling innovation. They must participate in international standard-setting to ensure their interests are represented in the emerging global framework. And they must educate citizens about the implications of different custody models for their financial security and privacy.

Conclusion: Redefining Sovereign Power for the Digital Age

The transition from monetary issuance to asset custody as the primary expression of sovereign financial power represents one of the most significant transformations in the relationship between states and money since the abandonment of commodity standards. This is not merely a technological change but a fundamental reconceptualization of what financial sovereignty means in an increasingly digital and interconnected world.

Traditional monetary sovereignty—the exclusive right to issue currency and regulate its supply—remains important, but it is no longer sufficient to ensure a nation’s control over its economic destiny. As value increasingly exists in digital forms, as assets tokenize and migrate to blockchain networks, and as individuals gain the technical capability to custody their own wealth outside institutional frameworks, the question of who controls digital asset infrastructure becomes paramount.

States that successfully navigate this transition will be those that recognize custody sovereignty as a new imperative, invest in the necessary infrastructure and regulatory frameworks, and balance the competing demands of control and innovation. They will need to harness technology to enhance their capabilities while respecting the privacy and autonomy that citizens increasingly expect. They will need to cooperate internationally while protecting their particular interests.

The winners in this transformation will not necessarily be those with the largest economies or the most powerful militaries, but those with the most robust, secure, and user-friendly digital financial infrastructure. As the nature of assets evolves and the mechanisms of custody transform, so too must our understanding of sovereignty itself. The power to issue currency is giving way to the power to secure, validate, and control digital assets—and this transition will shape the global balance of power for generations to come.

In this new paradigm, sovereignty is earned through providing valuable services—secure custody, reliable infrastructure, clear legal frameworks, and efficient settlement systems—rather than merely asserted through legal monopoly. Nations that embrace this reality and adapt their institutions accordingly will thrive in the digital age. Those that cling to outdated models of monetary sovereignty risk finding themselves increasingly irrelevant in a world where value flows through channels they neither control nor fully understand.

The shift from monetary issuance to asset custody sovereignty is not complete, nor is its ultimate form predetermined. The decisions made by policymakers, businesses, and citizens in the coming years will determine whether this transformation enhances or diminishes individual liberty, whether it concentrates or distributes power, and whether it serves the interests of the many or the few. What is certain is that we cannot go back to the world where state monopoly on currency issuance alone guaranteed financial sovereignty. The future belongs to those who master the new domain of digital asset custody and control.