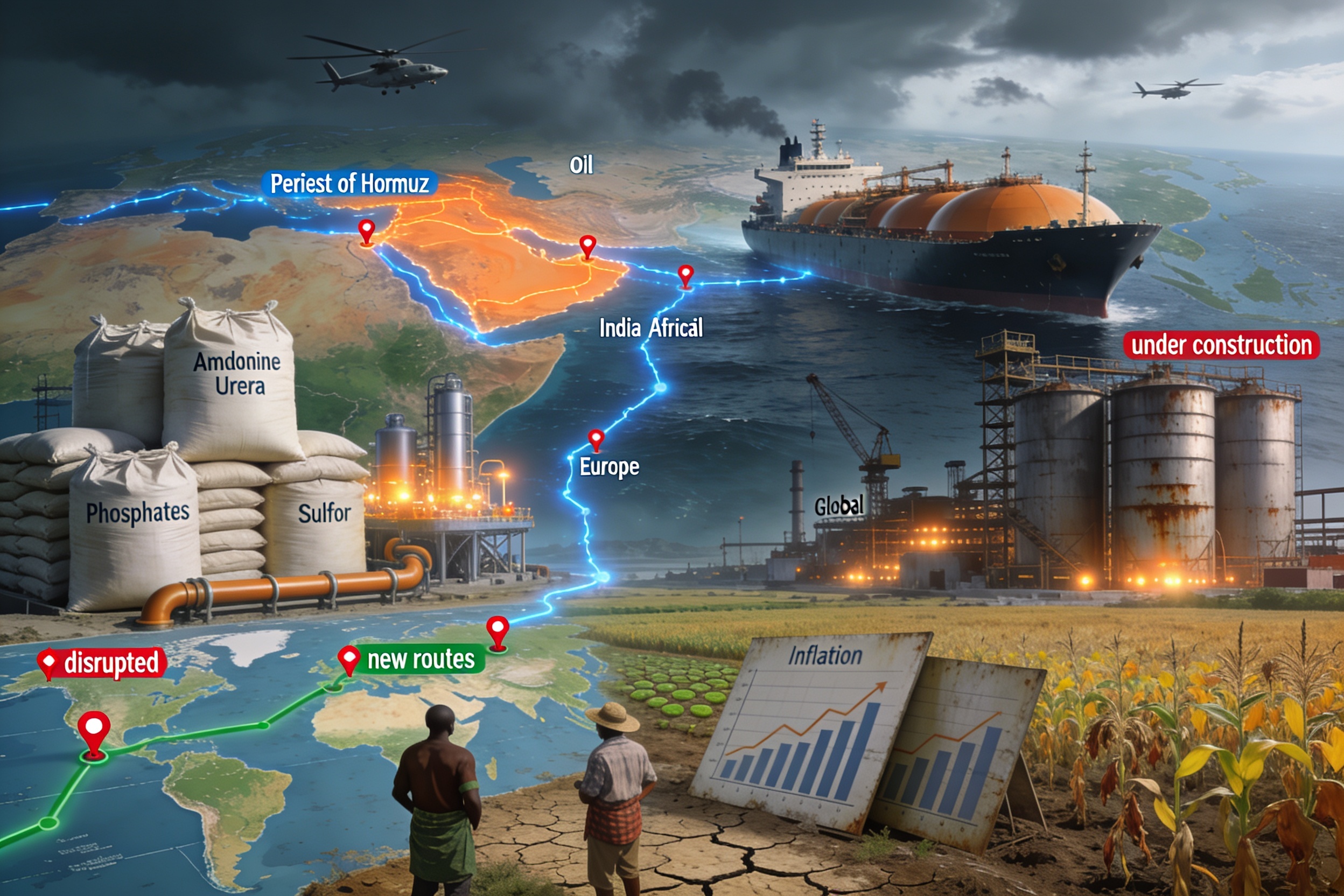

Restrictions on navigation through the Strait of Hormuz have led to an increase in the price of oil and its derivatives, including fertilizers used worldwide in agriculture. Higher prices discourage fertilizer use, which in turn leads to reduced agricultural production.

Most vulnerable countries—with low agricultural productivity and high dependence on imported inputs such as fertilizers—rely on exports from the Persian Gulf and are located in Africa and South Asia.

Since fertilizer prices respond sensitively to supply and trade shocks, it is necessary to consider ways to increase the resilience of other markets by diversifying production globally.

The current shock in the supply of oil and its derivatives is not the first in recent decades, but follows two other events that disrupted global supply chains: the Covid-19 pandemic (2020–2021) and the war in Ukraine (from 2022 onward). In response to the conflict in Ukraine, the United States and the European Union imposed a series of sanctions that affected exports of oil and derivatives from Russia and Belarus.

Regarding the crisis in the Persian Gulf and the closure of the Strait of Hormuz by Iran, declared in March 2026, the authors note that approximately 30% of global fertilizer trade passed through this region, along with 20% of liquefied natural gas (LNG) and 27% of oil.

In terms of fertilizers, from 2023 to 2025, Gulf countries were the world’s largest exporters of ammonia and urea—both nitrogen-based compounds—and the second largest exporters of diammonium phosphate (DAP) and monoammonium phosphate (MAP). Gulf LNG exports are vital for fertilizer production in other countries with limited domestic natural gas supply, including India, Pakistan, Bangladesh, and Turkey.

Ammonia is the basic input for all nitrogen fertilizers and is produced using LNG. Qatar, located in the Gulf, is the world’s third-largest LNG exporter, after the United States and Australia. Between 2023 and 2025, 29% of ammonia exports originated from the Gulf, with India, South Korea, Morocco, Japan, South Africa, and the United States as the main importers.

As for urea, during the same period, Gulf exports accounted for 36% of the global total, with India, Brazil, Thailand, the United States, and Turkey as the main importers. Iran holds a prominent position in this market, according to the International Fertilizer Association.

Regarding phosphates, the Gulf accounts for 26% of DAP exports and 13% of MAP exports. Saudi Arabia is the largest producer, while India, the United States, Brazil, and Australia are the largest buyers.

Sulfur, the basis for sulfuric acid, is obtained as a byproduct of oil refining and is an extremely important substance not only for the fertilizer sector but also for the mining and pharmaceutical industries. The Middle East is responsible for half of global production, much of which is transported through the Strait of Hormuz to markets as diverse as the United States, China, India, and Indonesia.

Faced with the production crisis due to transportation blockages in the Gulf, countries have adopted different strategies and have been affected in distinct ways:

- The United States, directly involved in the conflict, is less affected than other major markets, since 65% of its consumption is produced domestically. Even so, it has eased sanctions on Russian oil and derivatives, as well as Belarusian potash.

- In Europe, farmers—highly dependent on subsidies—have requested support from governments and European Union institutions.

- In India, producers have called for increased subsidies and greater investment within the oil and gas industry for the fertilizer sector.

- African countries have been especially vulnerable in their agricultural sector, as fertilizer consumption fell by 25% compared to 2022 following the outbreak of the war in Ukraine.

Although the crisis could be resolved through a peace agreement involving the United States, Israel, and Iran—or at least by ending hostilities and missile exchanges between the latter two countries—the major risk for global food production lies in a prolonged increase in fertilizer prices, during a period still insufficient for investments in the sector to mature in other regions closer to major consumers.

This price increase thus becomes a risk factor for declining production, rising food prices, and, consequently, increasing global hunger.

Brazil, the largest agricultural power in what may be called the Global South, finds itself in a particularly uncomfortable position, as it produces only 15% of the fertilizers it consumes, remaining dependent on producer markets in the Middle East, as well as Russia and Belarus. The crisis in global fertilizer supply could threaten Brazil’s position as one of the world’s major food suppliers if the crisis in Hormuz persists throughout 2026.

In this context, given supply shocks in a world moving toward a “post-globalization” scenario, countries—especially in the Global South—must develop strategies for economic self-sufficiency, reducing dependence on imports of critical inputs such as fertilizers, which are now as essential as water and energy due to modern agriculture’s reliance on them. It is necessary to consider industrial policies aimed at building production chains within major consumer markets to prevent a decline in global food production.

Reference:

“The Iran war’s impacts on global fertilizer markets and food production,” by Charlotte Hebebrand, Joseph Glauber, Rob Vos, and Brendan Rice, International Food Policy Research Institute (IFPRI).